Moving to a high-cost city for a tech or finance role means your salary calculation gets much more complicated than a simple pay stub back home. Countries use unique tax rules, allowances, and employer payroll models that can dramatically change your take-home pay. Understanding each method and how factors like progressive tax brackets or the Dutch 30% ruling affect your real earnings is crucial. This guide breaks down the key expat salary calculation methods and explains what every relocating professional needs to know to accurately evaluate compensation across borders.

Table of Contents

- Defining Expat Salary Calculation Methods

- How Tax Rules Shape Your Calculation

- Allowances and Compensation Structures

- Salary Models: Home, Host, Split, Shadow

- Home Country Model: The Stability Play

- Host Country Model: Going All In

- Split Salary Model: Hedging Your Bets

- Shadow Payroll Model: Tax Compliance Without Disruption

- Choosing Your Model

- How Net Pay Is Determined Worldwide

- The Tax System Foundation

- How International Organizations Calculate Net Pay

- Regional Deduction Variations

- Taxes, Social Security, and Legal Rules

- How Progressive Tax Systems Work

- Social Security Contributions: The Hidden Deduction

- Special Tax Provisions for Expats

- Legal Compliance Obligations

- Currency, Allowances, and Living Costs

- Understanding Currency Risk and Split Pay

- Cost-of-Living Allowances: Why They Matter

- Evaluating Real Purchasing Power

- Negotiating Allowances Effectively

- Common Mistakes and How to Avoid Them

- Underestimating Living Costs and Banking Inefficiency

- Missing Tax Deductions and Allowable Benefits

- Money Transfer and Exchange Rate Negligence

- Legal and Compliance Oversights

- Inadequate Emergency Planning

Key Takeaways

| Point | Details |

|---|---|

| Understand Salary Calculation Methods | Different countries utilize varied approaches for expat salary calculations. Grasping methods like gross, net, and tax-optimized salaries is vital for accurate compensation assessment. |

| Research Tax Obligations | Familiarize yourself with local tax systems, as tax rates and obligations differ significantly between countries and can impact overall take-home pay. |

| Negotiate Allowances Strategically | Always consider additional allowances such as housing and cost-of-living adjustments when evaluating job offers, as they can significantly affect your financial wellbeing. |

| Plan for Currency and Living Costs | Recognize how currency fluctuations and cost of living discrepancies can affect your net pay; detailed budgeting is crucial to ensure financial sustainability abroad. |

Defining Expat Salary Calculation Methods

Expat salary calculation isn't a one-size-fits-all formula. The moment you accept a job overseas, your compensation structure becomes dramatically different from what you'd earn at home. The challenge is that multiple calculation methods exist across different countries, each with unique tax rules, allowances, and deductions that directly impact your take-home pay.

When relocating for work, you'll encounter several primary approaches to determining your actual earnings:

- Gross salary approach: Your employer states a total annual compensation before any taxes or deductions

- Net salary approach: The amount you actually receive after all taxes, social security contributions, and mandatory deductions

- Tax-optimized salary approach: Structured to maximize benefits like housing allowances or tax-advantaged compensation methods

- Currency-adjusted salary approach: Compensation calculated in your home country's currency but paid in your destination country's currency

The distinction matters enormously. Two expats earning the same gross salary in different cities might take home 30-40% different amounts depending on tax structures and available allowances.

How Tax Rules Shape Your Calculation

Tax systems vary wildly between countries, and understanding how they work is non-negotiable. Some nations offer specialized provisions designed specifically for relocating professionals. For example, the Dutch 30% ruling tax facility allows employers to compensate expats by paying a portion of wages tax-free, which substantially reduces your taxable income during the eligibility period. This type of incentive directly affects how you should calculate and negotiate your salary.

Other countries implement progressive tax brackets where your rate increases with income, while some use flat-tax systems. Understanding these differences means the difference between expecting a certain take-home amount and being surprised when your first paycheck arrives.

Different countries structure salary calculations through vastly different tax methods—what works in one city becomes irrelevant in another, making location-specific research absolutely critical before accepting any offer.

Beyond income tax, you'll navigate social security contributions (often 5-15% of gross salary), healthcare deductions, and sometimes mandatory pension contributions. Remote workers and digital nomads face additional complexity because they may be classified as independent contractors rather than employees, which changes the entire calculation methodology.

Allowances and Compensation Structures

Many international employers use allowances to structure expat compensation more favorably. These might include:

- Housing allowances: A separate payment covering rent, often calculated as a percentage of salary or fixed amount

- Cost-of-living adjustments: Additional compensation reflecting higher expenses in expensive cities

- Tax-equalization payments: Your employer covers the difference between home and host country taxes

- Relocation assistance: One-time or ongoing payments for moving and settling costs

- Educational allowances: For employees with school-age children relocating abroad

These aren't bonuses—they're structured salary components that fundamentally change how you calculate your actual compensation. A job offering $120,000 gross salary with a $30,000 housing allowance functions very differently from a $150,000 straight salary in an expensive city.

The critical insight here is that your gross number tells only part of the story. You need to separate base compensation from allowances and understand which components are taxable in your destination country. Some countries tax housing allowances; others don't. Some allow you to claim housing costs as deductions; others forbid it entirely.

When you're evaluating offers from different cities, using a platform that accounts for how net salary actually gets calculated abroad becomes essential rather than optional. The math changes based on tax brackets, available deductions, and local regulations in ways that simple percentage calculations can't capture.

Pro tip: Request your potential employer provide a detailed breakdown showing gross salary, each allowance separately, estimated taxes, and projected take-home pay for your specific destination—this removes guesswork and prevents nasty surprises when you're already relocated.

Salary Models: Home, Host, Split, Shadow

Your employer has multiple ways to structure and pay your international salary, and each method carries different tax and financial implications. Understanding these models is crucial because they determine not just how much you receive, but when you receive it, in which currency, and what tax obligations you'll face in each country. The model your company chooses affects everything from your cash flow to your long-term financial planning.

The four primary salary models each solve different problems for international employers and employees:

- Home country model: You remain on your home country payroll with all salary and taxes handled there, even though you work abroad

- Host country model: Your employer transfers you entirely to the host country payroll system with local employment contracts and tax obligations

- Split salary model: Your compensation divides between home and host country payments, with portions processed through each jurisdiction's payroll

- Shadow payroll model: You receive payment from one location while a parallel payroll system tracks obligations in another jurisdiction for tax compliance

Each approach creates different outcomes for your take-home pay, retirement contributions, and tax liabilities. What works brilliantly for a six-month assignment might create nightmares for a three-year relocation.

Here's a comparison of the four main expat salary models and their impact on employment:

| Salary Model | Payroll Location | Tax Complexity Level | Employment Stability |

|---|---|---|---|

| Home Country Model | Home country only | High, dual obligations | High for short stays |

| Host Country Model | Host country only | Moderate, local only | Lower for home benefits |

| Split Salary Model | Both home and host | Very High, dual filings | Moderate for long-term |

| Shadow Payroll Model | Home with shadow in host | Very High, advanced compliance | High for global firms |

Home Country Model: The Stability Play

With the home country model, your employer keeps you on the home country payroll indefinitely, even though you're physically working abroad. Your salary gets processed through home country tax systems, and you typically maintain your home country employment contract. This approach offers psychological comfort and administrative simplicity for both employer and employee.

However, this model creates serious complications. You'll likely owe taxes in both your home country and your host country, and figuring out which government gets what becomes a headache. Most countries tax residents on worldwide income, so your host country will want taxes on your earnings regardless of where your paycheck originates. You'll end up paying taxes twice unless you qualify for foreign earned income exclusions or can claim tax credits.

The home country model works best for short-term assignments (under 12 months) or situations where you maintain primary residence at home. It breaks down fast for permanent relocations or multi-year assignments.

Host Country Model: Going All In

The host country model transfers you completely onto the host country payroll. Your employer in the destination country becomes your official employer, you sign a local employment contract, and all taxes flow through the host country system. This approach legally establishes you as a resident employee in that jurisdiction.

This model simplifies tax compliance because you report to only one country's tax authority. Your employer handles social security contributions, healthcare deductions, and pension requirements according to local law. The clean structure means fewer complications and lower accounting costs.

The tradeoff: you lose any home country employment protections, benefits continuity becomes murky, and you face currency risk if your home country income needs are significant. Some expats struggle with this because they feel genuinely disconnected from their home country employment systems.

Split Salary Model: Hedging Your Bets

The split salary model divides your compensation between your home country and your host country. Typically, your base salary remains on the home country payroll while allowances (housing, cost-of-living) get paid locally. This hybrid approach attempts to capture the benefits of both systems.

Split arrangements help manage currency exposure by paying some compensation in your home currency and some in the local currency. They also simplify some tax calculations by separating base pay from location-specific allowances. Many multinational companies prefer split models because they maintain headquarters employment relationships while accommodating local regulations.

The complexity is that you'll still file taxes in both jurisdictions, coordinate between two payroll systems, and deal with timing differences when the two countries process payments on different schedules. Salary split arrangements divide expatriate compensation to ease these currency and tax complexities, though they require careful management to optimize your outcome.

Shadow Payroll Model: Tax Compliance Without Disruption

The shadow payroll model is sophisticated infrastructure that most mid-level professionals don't encounter unless working for truly global organizations. Here's how it works: you receive your actual salary payment from your home country (or wherever your primary payroll operates), but your employer simultaneously maintains a "shadow" payroll in your host country that tracks tax obligations and social security contributions without direct cash flow.

This setup allows your employer to comply with local tax and labor laws without disrupting your actual payment stream. Shadow payrolls help comply with local tax reporting while facilitating tax equalization and protection measures across diverse jurisdictions. The employer essentially handles your host country obligations invisibly so you can maintain seamless payment.

The shadow model requires sophisticated accounting infrastructure and works best for companies with established operations and dedicated international payroll teams. Smaller organizations rarely use it because the setup costs and ongoing complexity aren't worth the benefit.

Your salary model determines not just your take-home amount, but your tax filing obligations, currency exposure, and financial planning complexity—choose or negotiate this decision as carefully as you negotiate the salary itself.

Choosing Your Model

Your employer typically decides the model based on their infrastructure, the assignment length, and local labor laws. However, you can negotiate within these constraints. For long-term relocations of 2+ years, push for the host country or split models because they're legally cleaner and reduce dual-tax complications. For shorter assignments under 12 months, the home country model makes more sense.

Understanding salary negotiation strategies for expats helps you advocate for the model that works best for your specific situation and timeline.

Pro tip: Before accepting any international offer, ask explicitly which salary model your employer will use and request a detailed breakdown showing how your compensation flows through each country's tax system—this prevents surprises and lets you accurately calculate your actual take-home pay.

How Net Pay Is Determined Worldwide

Net pay calculation is not a universal formula. The amount you actually receive in your bank account depends on dozens of variables that change from country to country, city to city, and sometimes even employer to employer. Understanding how net pay gets calculated in your destination is non-negotiable before accepting any international job offer.

The process starts with your gross salary, which is the total compensation your employer agrees to pay. From there, the deductions begin. Different countries subtract different amounts through taxes, social security contributions, healthcare premiums, and pension obligations. A $100,000 gross salary becomes wildly different net amounts depending on location. In some countries, you might take home 65% of gross. In others, you'll see only 50% or less.

The calculation involves three major components:

- Income tax: Progressive or flat rates that vary by country and often by income level

- Social contributions: Mandatory payments toward social security, unemployment insurance, and healthcare (typically 5-15% of gross)

- Allowances and deductions: Location-specific adjustments, pension contributions, union dues, or other mandatory withholdings

The order these deductions happen matters. Some countries calculate income tax on your gross salary before social contributions come out. Others reverse the sequence. This timing difference can shift your net pay by hundreds of dollars monthly.

The Tax System Foundation

Every country taxes income differently. Understanding your destination's approach is the foundation of accurate net pay calculation. The world uses essentially two systems: progressive tax brackets and flat tax systems.

Progressive systems, used in countries like Germany, Canada, and Australia, increase your tax rate as income rises. You might pay 15% on your first earnings tier but 42% on income above a certain threshold. This means your effective tax rate (average tax across all income) differs from your marginal rate (what you pay on the next dollar earned). For expats in mid-level tech and finance roles, progressive brackets often create effective rates of 35-45% on total compensation.

Flat tax systems, used in some Eastern European countries and Russia, apply the same percentage to all income regardless of amount. They seem simpler but often include fewer deductions and allowances than progressive systems.

Beyond income tax structure, you'll navigate social security contributions. These mandatory payments fund healthcare, unemployment insurance, pensions, and disability coverage. They typically range from 5-15% of gross salary, though some countries push higher. Your employer may pay a portion directly (employer contributions), which doesn't reduce your net pay but represents real costs factored into your total compensation package.

Net pay calculation is location-specific and formula-specific—the same gross salary produces dramatically different take-home amounts across cities, making generic salary calculators unreliable for relocating professionals.

How International Organizations Calculate Net Pay

Some expats work for truly global employers like the United Nations, which use standardized approaches to ensure fairness across duty stations. Global public sector structures incorporate base salary with various non-monetary benefits and adjustments for local economic contexts.

The UN approach exemplifies how sophisticated international employers handle net pay. They set a global base salary scale referenced to the highest national civil service salaries (currently the US Federal Civil Service), then apply post adjustment allowances that compensate for cost-of-living differences and currency fluctuations. This ensures staff in expensive cities like London or Tokyo maintain purchasing power equivalent to colleagues in lower-cost locations. The formula keeps net compensation equitable worldwide while accounting for regional tax regimes and mandatory contributions that vary dramatically by location.

Private companies rarely employ such systematic approaches. Most handle expat compensation inconsistently, relying on individual negotiation and local payroll compliance rather than global equity frameworks.

Regional Deduction Variations

The specific deductions applied to your salary depend entirely on your destination country. North American countries typically have straightforward federal income tax plus state or provincial tax, with social contributions lower than Europe. European countries layer more social contributions but sometimes offer more generous deductions and allowances. Asian countries vary dramatically—Singapore has minimal social contributions and low tax rates, while Japan combines high income tax with significant social contributions.

Mandatory pension contributions create major variations. Some countries require employers to contribute directly to retirement accounts, which reduces your gross taxable income. Others require employee contributions from your net pay. Still others offer no mandatory pension system at all. These differences compound over multi-year assignments.

Health insurance deductions vary wildly too. Some countries provide universal healthcare (funded through taxes or social contributions), so no separate deduction appears on your paycheck. Others require individual or employer health insurance premiums to come from your salary. Private expat health insurance typically costs $1,500-3,500 annually depending on coverage level and age.

Understanding your specific destination's tax structure, social contribution rates, and mandatory deductions prevents the shock of discovering your net pay is 30% lower than you calculated. Using a comprehensive tax calculator that accounts for your exact location and salary prevents these costly surprises.

Here is a quick overview of major deduction categories faced by expats in different world regions:

| Region | Income Tax Structure | Social Contributions | Typical Deductions |

|---|---|---|---|

| North America | Federal, state/province | Lower than Europe | Health, pension, union fees |

| Western Europe | Progressive, high rates | High, mandatory pension | Child, rent, transport |

| Asia | Varies widely | Low to high, location-based | Housing, healthcare, few |

| Middle East | Often no income tax | Minimal or none | Expat health insurance |

Pro tip: Request an official pay stub simulation from your prospective employer showing gross salary, each deduction itemized, and net take-home amount in your destination currency—this eliminates guesswork and ensures you're making decisions based on actual numbers rather than estimates.

Taxes, Social Security, and Legal Rules

Taxes and social security aren't optional considerations when relocating internationally—they're legally binding obligations that directly reduce your take-home pay and affect your residency status. Many mid-level professionals underestimate how dramatically these obligations differ across countries, leading to unpleasant surprises when the first paycheck arrives or tax season arrives. Understanding the legal framework in your destination is as important as negotiating the salary itself.

The three foundational rules that govern your financial obligations abroad are:

- Residency determines tax scope: Where you legally reside determines whether you're taxed on worldwide income or only local income

- Employer withholding is mandatory: Your employer must withhold taxes and social contributions before you receive payment, not as optional deductions

- Compliance is non-negotiable: Failing to understand or follow local tax rules creates legal liability, penalties, and potential deportation risk

Your residency status is the starting point. Most countries define residents as people who spend more than 183 days in the country annually (though this varies). Once classified as a resident, you typically face tax obligations on all worldwide income, regardless of where you earned it. This means a remote worker earning American dollars while living in Germany must declare that income to German authorities and pay German taxes on it.

How Progressive Tax Systems Work

Progressive tax brackets are the most common approach globally, used in countries like Germany, Canada, Australia, and most European nations. The system increases your effective tax rate as income rises, which sounds simple but creates real complexity when calculating net pay.

Here's the practical reality: if Germany's first tax bracket applies 15% tax on income up to €20,000, the next 25% on income from €20,001 to €50,000, and 42% on income above €50,000, your effective tax rate depends entirely on total income. Earn €60,000 gross and you pay roughly 28% effective tax, not 42%. This distinction matters because your employer might quote the marginal rate (42%) while you calculate based on effective rate (28%), creating a €8,400 difference in expected take-home pay.

Understanding tax brackets is essential for accurate salary calculations, especially in progressive systems where rates increase substantially with income. Social security contributions layer on top of income tax, typically ranging from 8-15% depending on country and contribution type.

Misunderstanding your destination's tax brackets and social contributions is the number one reason expats feel financially blindsided after relocating—precise calculation requires knowing both your effective tax rate and total social deduction percentage.

Social Security Contributions: The Hidden Deduction

Social security contributions fund healthcare, unemployment insurance, pensions, and disability coverage. They're mandatory in nearly every developed country and typically range from 5-15% of gross salary, though some countries push toward 20%. The critical detail most expats miss is that contributions are calculated on gross salary before income tax, meaning they reduce the amount subject to income tax while also reducing your net pay.

Some countries split contributions between employee and employer. Your portion comes directly from your paycheck, but the employer's portion (often 15-25% of your salary) represents real compensation cost that factors into your total package value. Understanding the full cost helps you negotiate accurately—a job offering "$100,000 salary" might actually cost the employer $115,000-120,000 when social contributions are included.

Pension contributions create major variations. Germany mandates both employee and employer contributions (about 18% combined). France similarly mandates pension contributions. Meanwhile, the United Kingdom relies more on individual pension savings with less mandatory contribution. Singapore has virtually no mandatory pension contribution, making gross salary much closer to take-home pay compared to European equivalents.

Special Tax Provisions for Expats

Some countries offer specialized tax advantages specifically designed to attract relocating professionals. The Netherlands' famous 30% ruling provides tax advantages for highly skilled migrants, allowing employers to pay up to 30% of wages tax-free (reducing to 27% in 2027) for up to five years. This ruling directly reduces your taxable income and alters social security contribution calculations, potentially increasing take-home pay by 5-8% compared to standard tax treatment.

Other countries offer similar provisions:

- Portugal: Non-habitual resident program offering reduced tax on foreign-source income for 10 years

- Switzerland: Cantonal tax negotiations for wealthy expats (varies dramatically by region)

- Japan: Special tax treatment for assignees under certain conditions

- UAE: No personal income tax on employment income (though other taxes apply)

These provisions often require specific eligibility criteria, employer sponsorship, and formal applications. Missing deadlines or misunderstanding eligibility costs thousands in lost tax savings.

Legal Compliance Obligations

Your legal obligation extends beyond paying taxes. Most countries require:

- Tax registration: Obtaining a local tax identification number

- Annual tax filing: Submitting income tax returns even if your employer withholds everything

- Residency declaration: Registering as a resident with local authorities within specific timeframes

- Healthcare enrollment: Registering with public healthcare or obtaining private insurance proof

- Pension fund registration: Ensuring contributions are properly directed to mandated pension accounts

Failure to comply creates compounding problems. Late tax filing incurs penalties (typically 5-10% of owed taxes). Unregistered employment can result in employer fines and personal liability. Some countries threaten employment visa revocation for tax non-compliance. For professionals in tech and finance, visa revocation essentially ends your assignment.

Pro tip: Hire a local tax accountant in your destination country within your first month—the €300-500 investment prevents costly mistakes on tax filings and ensures you're optimizing available deductions and special provisions specific to your situation.

Currency, Allowances, and Living Costs

A salary that looks impressive on paper can evaporate into inadequacy once you account for currency fluctuations, cost of living differences, and allowance structures. You might earn $120,000 in a high-cost city while your colleague earns $85,000 in a cheaper location, yet you both end up with similar purchasing power. Understanding how currency, allowances, and living costs interact is the difference between a financially sustainable relocation and one that drains your savings monthly.

Your salary calculation must account for three interconnected factors:

- Currency exposure: Which currencies you receive payment in and how exchange rate fluctuations affect your purchasing power

- Cost-of-living allowances: Adjustments employers add to base salary to reflect local price levels

- Living cost differences: The actual price gap between your home city and destination city for rent, groceries, transportation, and other essentials

These factors aren't theoretical—they directly determine whether your salary actually supports the lifestyle you expect or leaves you financially stressed despite earning a substantial gross amount.

Understanding Currency Risk and Split Pay

Currency risk is real and often ignored until exchange rates shift dramatically. If you earn a salary in Euros but have significant expenses in US dollars (like student loans or family support), a strong dollar means your expenses increase while your Euro-denominated salary stays flat. A 10% shift in exchange rates can cost you thousands annually.

This is why sophisticated employers use split pay arrangements. Split pay models divide salaries between home and host currencies to address currency risks and local living cost differences. The portion paid in host currency covers day-to-day expenses, while the home currency portion covers savings and non-spendable costs like insurance or family obligations.

Here's how split pay works in practice: an American employee relocating to London might receive 60% of salary in British pounds (for rent, food, transportation) and 40% in US dollars (for American student loans, home country insurance, or savings). This structure keeps your purchasing power stable despite exchange rate movements because your essential expenses match your currency exposure.

Without split pay, you face constant uncertainty. Exchange rate swings create budget anxiety and make financial planning nearly impossible. Most mid-sized companies don't offer split pay because it requires sophisticated payroll infrastructure, but multinational organizations increasingly recognize it as essential for expat retention.

Cost-of-Living Allowances: Why They Matter

Cost-of-living allowances (COLAs) are additional compensation your employer adds to base salary to reflect how much more expensive your destination is compared to a reference point (usually the home country or company headquarters). They're not bonuses—they're structured salary components designed to preserve your purchasing power.

A software engineer earning $100,000 base salary relocating from Austin, Texas to Zurich, Switzerland might receive a 35% COLA, bringing total compensation to $135,000. The additional $35,000 isn't a raise; it's compensation for the fact that rent, groceries, and dining in Zurich cost roughly 35% more than Austin. Without the COLA, your real purchasing power drops by a third despite the higher gross number.

COLAs vary based on:

- City pair: Some cities require 50%+ allowances (Hong Kong, Singapore, Zurich) while others add 5-10% (Eastern European cities)

- Assignment duration: Long-term assignments sometimes use adjusted COLAs; short-term assignments might use higher percentages

- Employment sector: Finance and tech often use more generous COLAs than other industries

- Family status: Allowances often increase if relocating with dependents

The critical distinction is understanding that COLAs are part of your salary, not separate benefits. When evaluating a job offer, add base salary plus COLA to understand your true compensation. A $100,000 base with 30% COLA equals $130,000 real compensation.

Evaluating Real Purchasing Power

Before accepting any international offer, you need to understand what your salary actually buys. A $150,000 salary sounds impressive until you realize rent consumes $3,500 monthly in your destination city, leaving $1,000 per month after housing and tax.

Cost-of-living differences dramatically shape whether a relocation makes financial sense. A salary that's reasonable in one city becomes inadequate in another despite being numerically identical. You must research actual costs in your destination for:

- Housing: Average rent for a one-bedroom apartment in a professional neighborhood

- Transportation: Public transit costs or car ownership expenses

- Groceries and dining: Supermarket prices versus restaurant costs

- Utilities and services: Internet, phone, gym, entertainment typical costs

- Healthcare: Insurance premiums and out-of-pocket medical costs

Multiply monthly costs by 12, add estimated taxes, and compare to your projected take-home pay. If the math doesn't work, the salary isn't competitive regardless of the gross number.

Currency exposure, COLA structures, and actual living costs are interconnected—evaluating salary offers without analyzing all three together creates costly financial blindness and preventable relocation regrets.

Negotiating Allowances Effectively

Allowances are negotiable, though most employers present them as fixed. When evaluating multiple offers, compare total compensation (base plus allowances) rather than base salary alone. If one employer offers $100,000 base with 20% COLA and another offers $110,000 base with 10% COLA, the first offer is actually more generous ($120,000 versus $121,000), though it looks weaker initially.

Negotiate allowances by:

- Requesting transparent COLA calculations: Ask how the employer determined the percentage and whether it's based on published cost-of-living indices

- Benchmarking against competitors: Research what other companies offer for similar roles in your destination

- Documenting family circumstances: Additional dependents justify higher allowances; provide evidence if applicable

- Discussing duration adjustments: Ask whether allowances change if your assignment extends beyond initial terms

Allowances often increase annually based on inflation indices, but not always. Confirm the COLA adjustment mechanism before signing your contract.

Pro tip: Before accepting any relocation offer, calculate monthly living costs in your destination and compare against your projected monthly take-home pay after all taxes and social contributions—if housing alone consumes more than 30-35% of net pay, the salary is insufficient regardless of how impressive the gross number appears.

Common Mistakes and How to Avoid Them

Expats make predictable financial errors that cost thousands of dollars annually. These aren't mistakes from ignorance—they're mistakes from assumptions. You assume your home country banking practices work abroad. You assume your salary calculation is accurate without verification. You assume legal compliance happens automatically. By the time you realize these assumptions were wrong, months have passed and damage is done. Understanding the most common pitfalls lets you avoid the expensive lessons others learned the hard way.

The pattern is consistent across relocating professionals: initial excitement masks financial blind spots, and small oversights compound into significant problems. A typical expat might overpay banking fees by 40% for six months, miss out on applicable tax deductions worth $3,000 annually, and fail to optimize allowance structures by $8,000 yearly. Combined, that's nearly $30,000 in preventable losses over three years.

Underestimating Living Costs and Banking Inefficiency

The first major mistake is inadequate cost-of-living research. Many relocating professionals base their budgets on general country data rather than neighborhood-specific costs in their destination city. A tech worker accepting a job in Singapore might assume the "average" cost of living without researching that Marina Bay condominiums cost 40-60% more than Jurong neighborhoods. The salary looked sufficient until month two when actual housing bills arrived.

Related to this is the banking mistake. Continuing to use your home country bank account for daily expenses in your destination country creates unnecessary fees. International transfer charges, currency conversion markup, and monthly maintenance fees stack quickly. Common expat financial mistakes include using foreign bank accounts too long, leading to excessive transaction fees that could easily total $2,000-3,000 annually.

The solution is straightforward but requires action: open a local bank account in your destination within your first month. Most countries allow expats to open accounts with an employment contract and passport. Local accounts eliminate currency conversion fees, reduce transfer costs, and provide access to local payment systems (essential for rent, utilities, and grocery payments). The $50-100 administrative cost pays for itself within two months through fee savings.

Missing Tax Deductions and Allowable Benefits

Second major mistake: failing to claim available deductions and allowances. Governments and employers offer benefits that expats miss simply because they don't know they exist. In the Netherlands, expats might qualify for child allowances, healthcare subsidies, or specific deductions for relocating costs. These benefits aren't automatically applied—you must research eligibility and submit applications within specific timeframes.

Similarly, many expats don't negotiate or claim housing allowances they're entitled to. Your employment contract might include provisions for housing support that you overlook because you didn't ask. Others receive allowances but fail to understand tax treatment—in some countries housing allowances are taxable income; in others they're partially or fully tax-exempt. Not understanding this difference means overpaying taxes by $2,000-5,000 annually.

The solution requires proactive research and documentation:

- Within week one: Request a written summary from your employer stating all compensation components including allowances

- Within month one: Schedule a consultation with a local tax professional to identify available deductions

- Ongoing: Set calendar reminders for benefit application deadlines (often January for annual benefits)

This investment of a few hours prevents thousands in lost savings.

Money Transfer and Exchange Rate Negligence

Ignoring exchange rates and transfer costs creates silent financial drain. When sending money home or converting currencies, many expats use whatever service is convenient rather than cost-effective. Bank transfers might cost 4-5% in fees and unfavorable exchange rates. Specialized money transfer services might charge only 1-2%. Over a year, sending $10,000 home quarterly means paying $400-2,000 more than necessary depending on method chosen.

Failing to research money transfer costs and exchange rates leads to preventable financial loss during remittances. The solution is comparing providers before opening any accounts. Services like Wise, OFX, or Remitly often offer better rates than traditional banks, particularly for amounts over $5,000.

The costliest expat mistakes aren't about salary negotiation—they're about the small financial decisions made after relocation, compounding into thousands of dollars lost through inefficiency and ignorance.

Legal and Compliance Oversights

Third major mistake: neglecting legal compliance obligations. This includes failing to register for local tax identification, missing residency declaration deadlines, or not understanding visa implications of employment changes. These aren't victimless errors—penalties for late tax registration can reach 10-15% of owed taxes, and visa non-compliance creates deportation risk.

Many expats also fail to maintain proper documentation. Keep records of:

- Employment contracts with compensation details

- Pay stubs showing all deductions

- Tax returns filed in both home and host countries

- Proof of residency status

- Healthcare and insurance documentation

- Pension fund statements and contribution records

Missing documentation during tax audits creates enormous problems. You might have paid correct taxes but lack proof, forcing re-payment while disputes resolve.

Inadequate Emergency Planning

Final mistake: insufficient emergency financial reserves. Expatriate life carries unique risks—unexpected job loss, visa revocation, or family emergencies requiring immediate travel. Many expats maintain the same emergency fund they had at home (three months' expenses) despite being in a less stable situation. International relocation requires six months' expenses in accessible reserves—enough to cover living costs if employment ends while managing visa and travel complications.

Without adequate reserves, a minor crisis becomes catastrophic. A job loss forces you to leave the country mid-contract, breaking leases and losing deposits. A family emergency requires expensive flights home, but you lack accessible funds because your salary is committed to monthly expenses.

Pro tip: Within your first month abroad, complete three essential tasks: open a local bank account, schedule a consultation with a tax professional, and verify all compensation components in writing from your employer—these three actions prevent the vast majority of common expat financial mistakes.

Master Your Expat Salary Calculation with Confidence

Navigating the complex world of expat salary models and international tax obligations can feel overwhelming. This article highlights crucial challenges like understanding gross vs. net salaries, tax jurisdictions, social security deductions, and managing currency risks that can drastically affect your take-home pay. If you want to avoid surprises and costly miscalculations when relocating abroad, you need transparent, data-driven insights tailored to your destination.

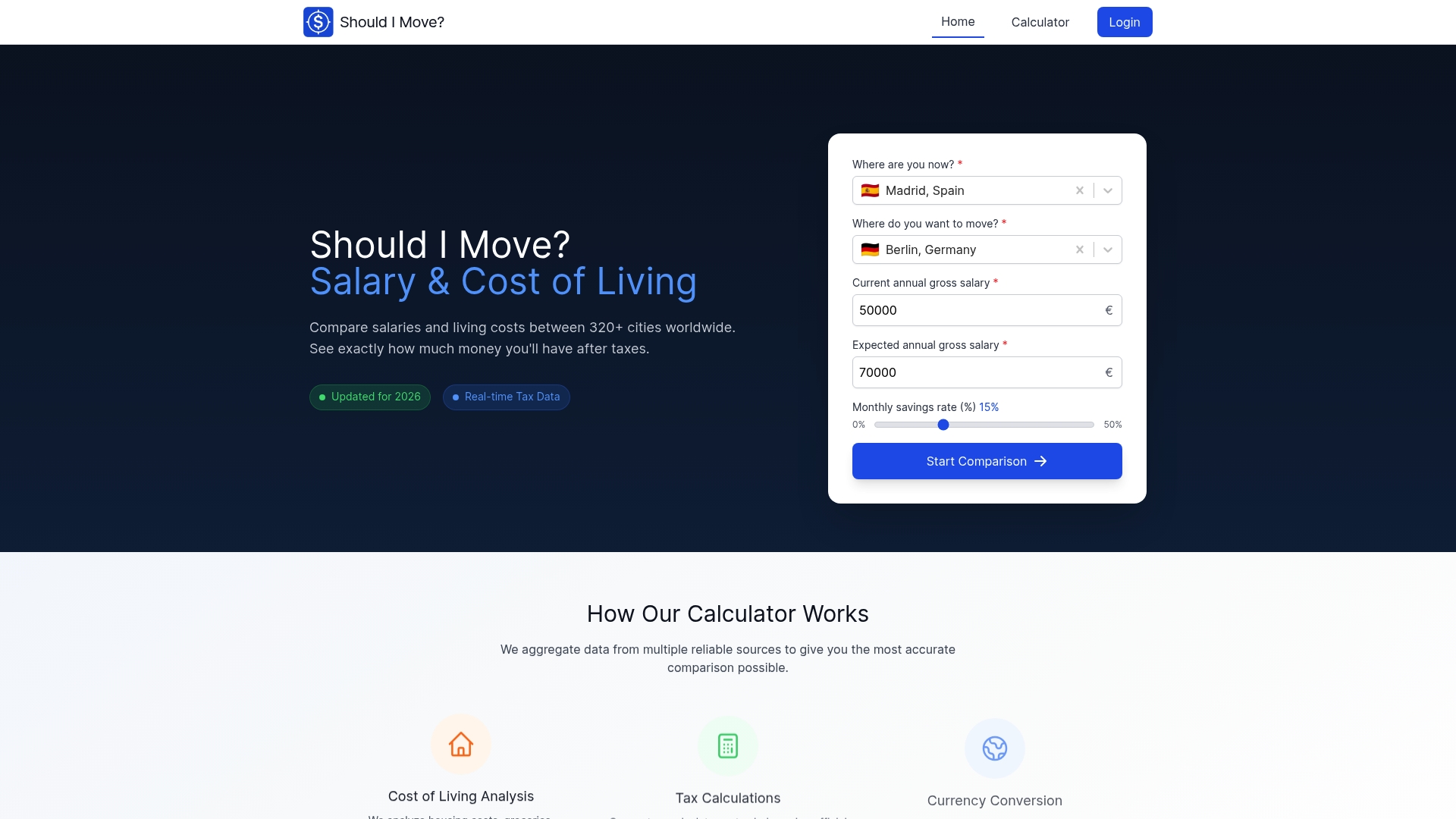

Take control of your financial future by using ShouldIMove.co to access precise net salary calculations, cost-of-living comparisons, and real-time currency adjustments across over 320 cities worldwide. Our platform helps you interpret complicated salary structures including split salary models, allowances, and tax deductions so you can confidently negotiate and optimize your expat compensation. Don’t leave your relocation budget to chance—start your personalized financial comparison now at ShouldIMove.co and make informed decisions that truly reflect your new life abroad.

Frequently Asked Questions

What are the primary methods for calculating expat salaries?

Expat salaries can be calculated using various approaches including the gross salary approach, net salary approach, tax-optimized salary approach, and currency-adjusted salary approach. Each method impacts your take-home pay differently based on tax rules and compensation structures.

How do tax rules affect my expat salary calculation?

Tax systems vary significantly from country to country, affecting your take-home pay. Understanding local tax provisions, progressive tax brackets, and any expatriate-specific incentives is crucial for accurate salary negotiation and calculations.

What types of allowances should I look for in an expat compensation package?

Common allowances in expat compensation packages include housing allowances, cost-of-living adjustments, tax-equalization payments, relocation assistance, and educational allowances for children. These can substantially impact your overall compensation and net pay.

What are the main salary models for expatriates?

The primary salary models include the home country model, host country model, split salary model, and shadow payroll model. Each has different implications for tax obligations, payment methods, and overall compensation, affecting your financial planning as an expat.

Recommended

- How to Calculate Net Salary Abroad – A Step-by-Step Guide for Expats | ShouldIMove

- 7 Things to Keep in Mind When Negotiating Salary as an Expat or Remote Worker | ShouldIMove

- Cost of Living – How It Shapes Relocation Decisions | ShouldIMove

- Blog – Cost of Living & Salary Guides | ShouldIMove

- 7 Key Tips for Comparing Renting vs Buying Your First Home - Finblog

- Let's Talk About Your Income - Mortgage Managers